A regional bank processed wire transfers using 1990s-era software that crashed twice a week. Engineers built a buffer system that caught wire requests from modern apps, validated them, and then fed them slowly into the old system during stable hours. The bank reduced wire transfer failures from 12% to 2% over six months. Three full-time engineers now babysit the connection between new and old systems every day, ensuring system compatibility. You can schedule a call with us to discuss B2B fintech solutions.

Why Do Banks Still Run on 40-Year-Old Code?

Banks know their systems are old. They know better options exist. Yet replacing core infrastructure could shut down financial institutions' operations for months.

What Are Legacy Systems?

Legacy systems keep banks running on financial software from the Reagan era. These mainframes process customer deposits and loan payments every day. Programmers wrote this code when computers filled entire rooms. The languages these systems speak died out years ago. Most current developers have never seen COBOL or worked with punch card logic.

Why Banks Keep Ancient Financial Technology

Replacing core banking fintech technology can be fatal to a business overnight. One foul line of new code might freeze every customer account. Banks lose money every second their systems go down. Replacement projects cost hundreds of millions and take years to complete. Regulators demand extensive integration testing before banks can switch to new platforms.

Common Legacy Systems in Finance

- Core banking platforms manage checking accounts and savings through 1980s databases.

- Payment systems move wire transfers using networks older than the internet.

- Trading platforms use stock purchases with proprietary code that only senior programmers understand.

- Credit systems approve loans through decision trees built years ago.

- Compliance systems generate regulatory reports in formats that predate Excel and lack platform scalability.

Bank Data Analytics Platform

They've had a quick grasp of what we are trying to do and delivered to our spec without a fuss.

What Breaks When You Connect New B2B Fintech Solutions to Old Banks?

Integration projects fail more often than they succeed, and the reasons are predictable.

When Old Meets New

Modern APIs expect JSON responses in milliseconds. Legacy systems return data in fixed-width text files that arrive hours after the event. The two sides use different network protocols and incompatible data formats. Developers spend months building translation layers that convert between systems that were never meant to work together, requiring service-oriented architecture and microservices frameworks.

Security Holes Everywhere

Banks face federal audits if customer data leaks during integration. Legacy systems lack modern encryption and access controls. Adding new connections creates more attack surfaces that hackers can exploit. Fraud detection becomes critical as compliance teams demand extensive security reviews, which delay projects by months.

Speed Limits Built In

Legacy mainframes process financial transactions in batches overnight. Modern apps, especially mobile banking services and SaaS solutions, need real-time processing for thousands of concurrent users. The old infrastructure becomes the limiting factor for the entire system. Peak traffic can crash legacy components that worked fine for decades.

Breaking Live Systems

Banks lose millions per hour when core systems go offline. Integration work requires touching live production environments. One configuration error can freeze customer accounts nationwide. Most banks schedule implementation windows at 3 AM on weekends to minimize exposure.

Code That Nobody Understands

Each integration adds complexity to systems that are hard to understand. Documentation for legacy code often exists only in the heads of senior developers. New features pile on top of old workarounds that nobody wants to touch. The codebase becomes more fragile with every change, weakening operational efficiency.

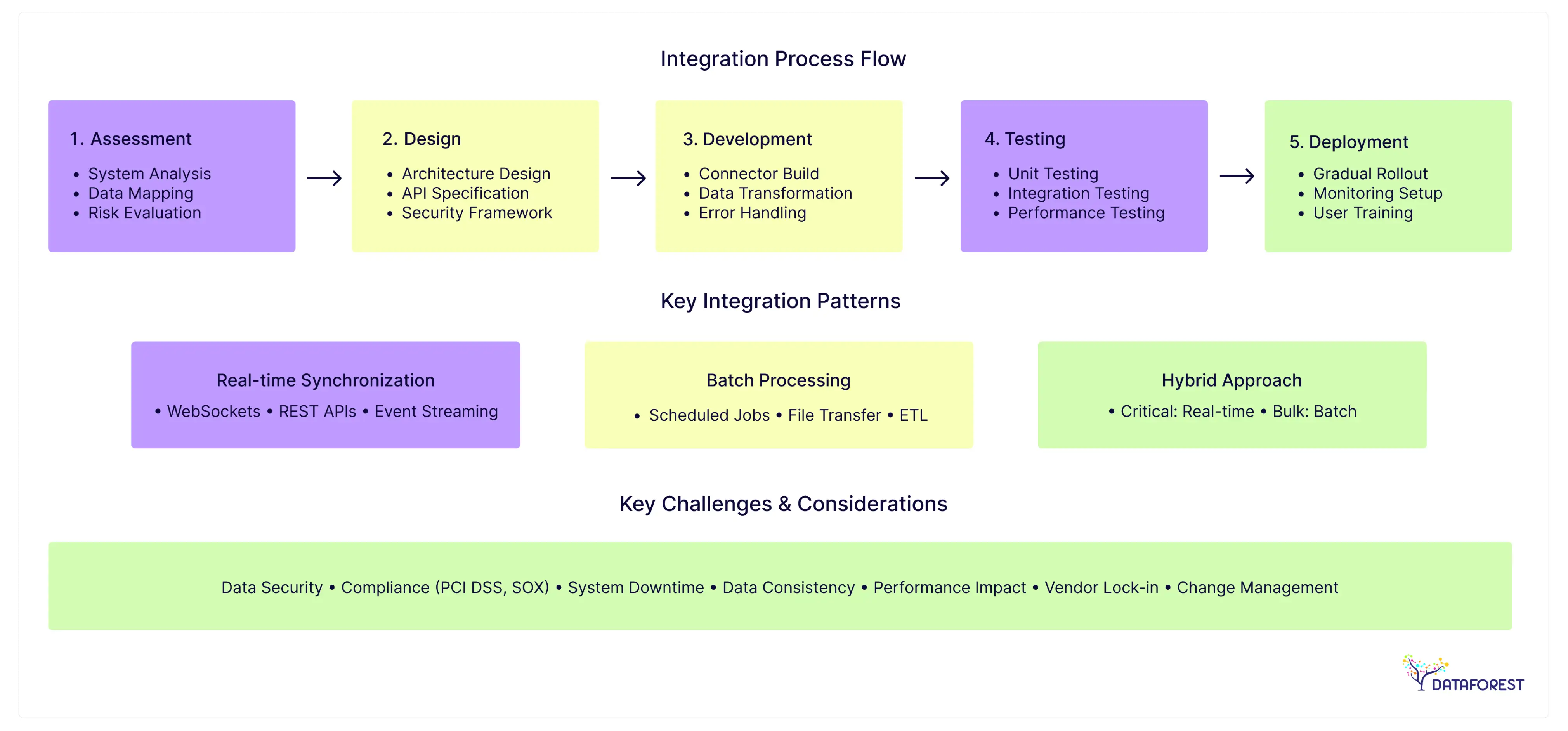

How to Fix Integration Projects That Keep Failing?

Integration attempts die from poor planning. Teams rush into technical work without understanding what breaks first. Success requires boring preparation and realistic timelines.

Map the Minefield First

Teams guess at what legacy systems contain instead of looking. The audit maps every database table, API integration endpoint, and batch job that touches customer data. Hidden dependencies surface during this process—connections between systems that nobody documented. Without the audit, integration attempts hit walls that could have been spotted months earlier through big data mapping and integration testing.

Building Translation Layers Between Systems

Middleware handles the conversion work between incompatible systems. The gateway accepts JSON requests from new apps and converts them into formats that old systems understand. This keeps integration complexity contained instead of spread across multiple codebases. Teams can debug connection problems without touching decades-old banking software, improving user experience.

Connecting Systems One Step at a Time

Teams that try to integrate everything at once usually fail spectacularly. Competent developers connect individual features sequentially—customer lookups first, then account balances, then transaction history. Each successful connection builds confidence and reveals problems before they become disasters. When something breaks (and it will), you know exactly which piece caused the failure instead of hunting through ten interconnected systems.

Making Sure Data Survives the Move

Migration projects fail when teams assume that data will transfer cleanly between systems that store information in entirely different ways. You must test the migration on exact copies of production data first, because customer records from 1987 contain unusual formatting that breaks modern validation rules. Innovative teams run side-by-side comparisons for weeks, checking that every account balance and transaction history matches perfectly between old and new systems. The validation work usually takes three times longer than anyone expects, but finding a $50,000 missing deposit after go-live destroys more than project timelines.

Getting Lawyers and Auditors on Board Early

Security approvals often drag on for months because compliance teams need to review every connection point between systems. Banks face massive fines if customer data leaks during integration work, so they scrutinize every API call and data transfer protocol. The smart move is to get security architects involved during planning, rather than waiting until code review—they know which approaches will never pass an audit. Projects that treat compliance as an afterthought often fail when auditors discover problems three weeks before the launch date, disrupting the onboarding process of fintech solutions.

Working With People Who Know the System

Bank IT teams have war stories about every weird quirk in their legacy systems—they know which stored procedures crash under load and which data fields contain garbage from 1994. External developers who ignore this tribal knowledge end up reinventing solutions that already exist or building integrations that work great in testing but fail catastrophically in production. The bank engineers also control access to production environments, so keeping them satisfied determines whether you receive the necessary system access to test your work. Most importantly, these folks understand the political landscape around system changes—they know which executives will kill projects and which compliance officers will demand six months of additional documentation.

Book a call to stay ahead in technology with b2b fintech industry solutions.

Why Do Big Companies Keep Procrastinating on FinTech Solutions in B2B Upgrades?

Large businesses know their fintech ecosystem is falling behind. Companies that move first gain advantages that become harder for competitors to match. Meanwhile, customer expectations continue to rise while legacy infrastructure becomes increasingly expensive to maintain.

Driving Digital Transformation and Competitive Advantage

When you upgrade your payment systems with fintech innovation, you can suddenly do things your competitors can't. Your business can offer net-15 terms that change based on how customers pay, while the guy down the street still uses spreadsheets to track invoices. Customers notice this—when payments work smoothly, they assume you run everything else well, too. Old financial systems become roadblocks that stop you from launching new services or expanding into different markets. The businesses that upgrade first get ahead and stay ahead because word spreads about how much easier they are to work with.

Making Customers Want to Stay

Financial friction creates emotional baggage that customers carry into every future interaction with your business. When someone has to chase down a missing payment or wait three weeks for a refund, they remember that frustration months later during contract renewals. Modern B2B fintech integration eliminates these pain points by automating financial operations. Process automation ensures invoices, refunds, and transactions happen instantly. Customers tend to stick with vendors who invest in better fintech partnerships, making their financial lives easier.

Building Systems That Won't Break Tomorrow

Legacy financial systems get more expensive and fragile every year until they eventually break something important at the worst possible time. Innovative companies build integration capabilities that support blockchain technology, wealth management services, and new services industry standards. Companies that invest in flexible infrastructure with platform scalability and microservices adapt quickly when markets shift. It's like wiring a house: you install enough electrical capacity for future needs instead of today's requirements. Companies that wait too long get stuck explaining to investors why they can't capitalize on new opportunities because their payment systems are too old to support different currencies. The businesses that invest in flexible financial infrastructure can pivot quickly when market conditions change, while their competitors remain locked into outdated systems.

How Can DATAFOREST Solve Legacy System Challenges in B2B Fintech?

Deloitte outlines emerging disruptions in banking and capital markets through 2030, providing context for B2B fintech strategy planning. Here’s how DATAFOREST can assist when facing integration challenges with client legacy systems:

- Bridging old and new: DATAFOREST bridges legacy systems and modern applications using data transformation methods, API gateways, service-oriented architecture (SOA), and cloud computing connectors—ensuring seamless data flow across b2b fintech infrastructures.

- Custom integration: Our approach combines workflow analysis with AI-driven tools, creating bespoke, non-disruptive fintech solutions in b2b that preserve stability.

- Scalable and enduring: We offer ongoing support and adaptation for b2b fintech solutions, enabling gradual legacy modernization without disruption.

Please complete the form to get consulting on B2B fintech solutions.

FAQ On B2B Fintech Solutions

What security risks should businesses consider when integrating fintech solutions with legacy infrastructure?

Legacy systems carry outdated defenses that hackers know well. Once linked to modern fintech, the attack surface expands fast. Every connection point becomes a door that needs constant watching and patching.

What are the best practices for migrating data from legacy systems to modern fintech platforms?

A big-bang move risks losing control. Breaking migration into steps keeps errors small and visible. Always verify data at each stage before letting it flow forward for B2B fintech.

What role do APIs play in facilitating integration between B2B fintech solutions and legacy systems?

APIs cut through complexity by translating old formats into modern ones. They prevent the need for complete rebuilds. But they still demand strong governance, or the multichannel integration turns fragile.

What are the signs that a client’s legacy system needs modernization before fintech integration?

Frequent crashes eat up time and money. Scaling the system becomes painful with every new demand. If workarounds outnumber core features, the platform has already fallen behind its competitors in the B2B fintech space.

Can middleware solutions simplify the integration process for complex legacy systems in B2B fintech?

Middleware gives breathing space between old and new. It allows step-by-step connection instead of ripping everything apart. The trade-off is another layer to manage, which can slow decisions later.

How does B2B fintech improve financial operations for businesses?

Through automation, B2B fintech eliminates the tedious work that bogs down finance teams every month. Instead of manually matching invoices to payments or chasing down missing documentation, automated systems handle the grunt work while people focus on strategy and analysis. Companies using B2B fintech get paid faster, make fewer accounting mistakes, and build stronger relationships with customers who appreciate smooth financial interactions.

Why is legacy system integration important in B2B fintech projects?

Banks still rely on mainframe computers from the 1980s, and B2B fintech companies must speak their language to get anything done. You can't just ignore these old systems because they control the money - every wire transfer, ACH payment, and account balance flows through infrastructure that predates the internet. Smart B2B fintech integration seamlessly connects modern apps to traditional banking systems, preserving the benefits of both, and giving businesses the best of both worlds.

.webp)